Employee vs Independent Contractor: Compliance Guide

Many organisations struggle to distinguish between employees and contractors, creating significant hidden liabilities that often go unnoticed until an audit begins.

This issue matters now more than ever because regulators are intensifying audits as cross-border hiring and remote work models become the global standard. The consequences of inaction can be severe: misclassification leads to retrospective tax bills, social security arrears, and damaging legal claims.

In this guide, I’ll provide a clear framework for status determination and practical risk mitigation strategies to help you navigate these situations.

Key Takeaways

- Operational Reality Overrides Labels: Regulators prioritise how work is actually done over the title written in a contract.

- Primary Risk Indicators: The level of control you exert and how much a worker is integrated into your team are the main factors used to determine status.

- Burden of Proof: The employer, not the worker, carries the legal responsibility to prove that a classification is correct.

- Rising Penalties: Misclassification fines are increasing globally as authorities crack down on "tax leakage."

- Proactive Protection: Conducting regular internal audits is the most effective way to reduce long-term financial exposure.

Defining the Employee vs Independent Contractor

The core difference between an employee vs independent contractor lies in the daily reality of the relationship, not the title at the top of the contract. In the world of remote work, it is easy to assume that because someone is working from a laptop in another country, they are automatically a freelancer.

However, a genuine independent contractor operates as a separate business entity, providing specialised services with high autonomy. In contrast, an employee is integrated into your business, subject to your direct control, and entitled to a suite of statutory benefits.

Assessing Professional Independence

To get your classification right, you need to distinguish between a "contract for services" and a "contract of service." A contract for services is what you have with a b2b partner; they are a separate business providing a specific outcome. A contract of service is employment.

One of the most effective ways to test for independence is to look at business risk and profit opportunity. A true contractor shoulders their own financial risk. If they finish a project early, they might make more profit; if they make a mistake, they fix it on their own time and at their own expense.

Employees, generally, do not carry this risk. They are paid for their time regardless of the company’s profit margins or the specific costs of the tools they use. If your worker has no "skin in the game" and no opportunity to increase their own profit through efficiency, they are likely an employee.

Contractual vs Operational Reality

You might have a signed document that explicitly says "This is not an employment relationship," but to a tax inspector, that piece of paper holds very little weight. Regulators across the globe follow the "Substance over Form" principle. This means they look past the fancy legal labels to see what is actually happening on the shop floor (or the Slack channel).

If you call someone a contractor but treat them like a member of staff (onboarding them with your internal HR tools, giving them a company email, and making them sit through every internal performance review), the "contractor" label vanishes.

Tax authorities aren't interested in your intent; they are interested in the fact that you are managing someone as an integrated part of your workforce. To remain compliant, your operational habits must match your legal documentation. If there is a gap between how you work and what you’ve signed, the operational reality will win every time.

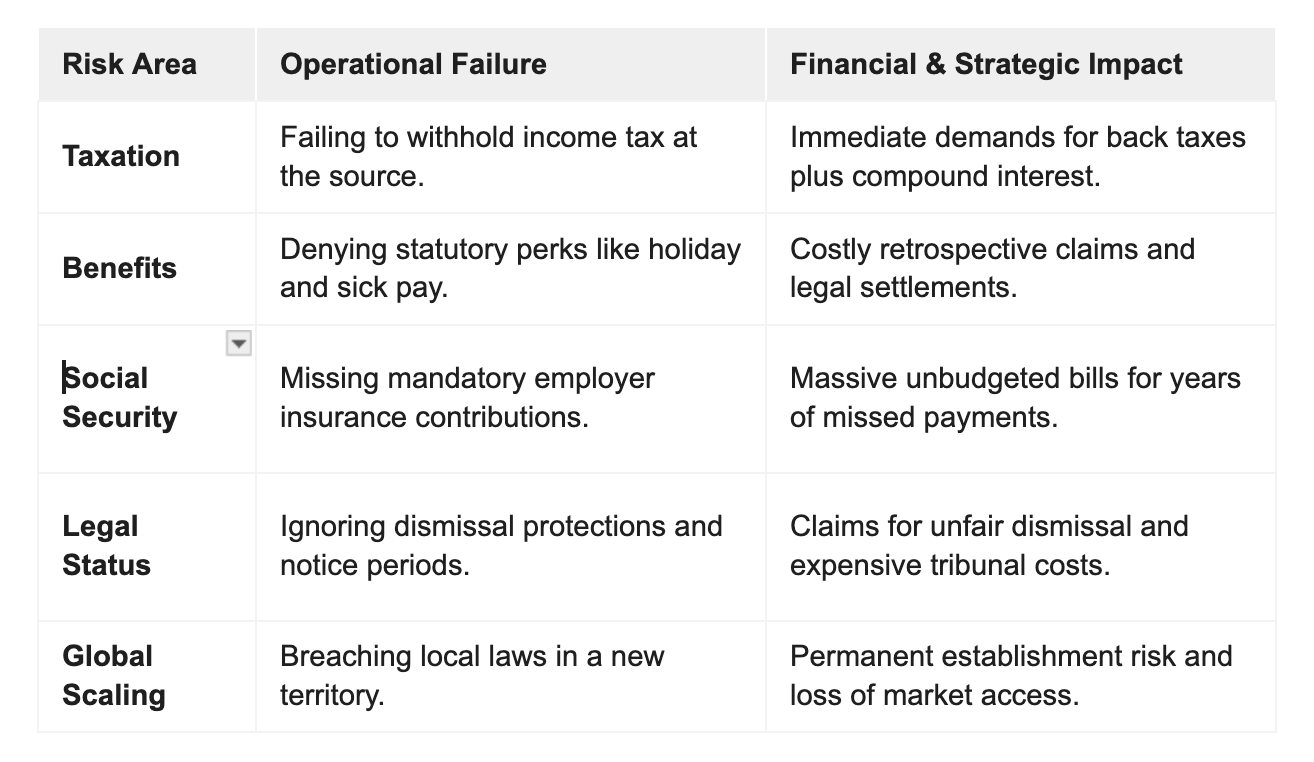

Why Misclassification Risk Matters

Misclassifying a worker creates an immediate financial threat because the hiring organisation is held strictly liable for all missed tax and social security contributions. In the eyes of the law, "we didn't know" is not a valid defence.

Authorities view misclassification as a loss of public revenue, and they expect the employer to make the treasury whole. This creates a "strict liability" scenario where the business must pay for the worker’s missing benefits, even if the worker originally agreed to the contractor status. As data-sharing between global tax offices increases, spotting these discrepancies has become a top priority for regulators.

These risks compound rapidly over time and across borders. A single misclassified worker in a remote team can act as a "tripwire," triggering a wider audit that exposes your entire organisation to multi-jurisdictional penalties.

What starts as a simple freelance agreement for a designer or developer can spiral into a multi-million-pound liability if the relationship "drifts" into employment territory. To stay safe, you must move beyond superficial contracts and ensure your operational reality matches the law. Getting this goes beyond “box-ticking” to protect your budget and your reputation from the ground up.

How to Assess Worker Status Correctly

To ensure accurate worker classification, you must look past the "freelancer" label and conduct a thorough compliance assessment. Authorities typically start with the "Control Test," which evaluates the level of authority you exert over when, where, and how a person works.

If you manage a contractor's daily tasks with the same granularity as a member of staff, you are likely assuming the legal risks of an employer. In the world of remote work, where digital oversight is constant, the line between "checking in" and "supervising" can become dangerously thin.

Measuring Direction and Control

Evaluating the level of supervision and performance management is the first step in any robust compliance assessment. A genuine contractor is an expert hired to deliver a specific outcome; they should decide the methodology themselves.

If your managers are providing step-by-step instructions, mandating specific "on-line" hours, or putting contractors through the same internal performance reviews as your employees, you are exercising "direction and control."

Another vital factor is "mutuality of obligation." This essentially asks: are you obliged to provide work, and is the worker obliged to accept it? If a contractor has a rolling expectation of steady work rather than a project with a defined start and end date, the relationship looks increasingly like employment. To keep things clean, focus on deliverables and avoid creating a culture where the worker is "on-call" for general tasks.

Integration and Equipment Tests

The "Integration Test" determines whether a worker is "part and parcel" of your organisation. If a contractor has a company email address, appears on your internal org chart, or has the authority to manage your permanent staff, they are deeply integrated into your business operations. From a regulator's perspective, if someone looks, talks, and acts like an employee, they are one.

Equipment also plays a significant role. While providing a company laptop might seem like a smart security move, it is a classic indicator of employment. Independent professionals are expected to provide their own "tools of the trade," including hardware, software licences, and insurance. When you provide the equipment, you are providing the means of production, which shifts the balance of the relationship. By keeping contractors at arm’s length (e.g., operating on their own systems and outside your core internal hierarchy) you significantly strengthen your compliance position.

Applying Status Tests in Real Scenarios

Regulators do not just read your contracts; they observe the "economic reality" of how your team functions.

The core question they ask is: "Does this person look and act like a business owner, or are they financially and operationally dependent on the hiring company?" In a world of borderless hiring, it is easy for lines to blur.

However, authorities look for specific indicators of independence that prove a worker is genuinely in business for themselves. If a worker cannot profit from their own efficiency or risk their own capital, they are likely an employee in the eyes of the law.

Moving from Uncertainty to Compliance

Independent contractor misclassification is rarely intentional, but it is one of the most common and costly compliance risks facing organisations with global workforces. As this guide has shown, regulators look beyond contracts to the practical reality of how work is performed. Without a proactive, evidence-based approach to assessment, operational drift can quietly turn legitimate contractor relationships into significant legal and financial liabilities.

I specialise in helping organisations assess contractor arrangements in practice and reduce risk before audits or claims arise. By reviewing how your workforce operates day-to-day, I provide clear, defensible guidance that supports compliant international growth. Get in touch to review your current contractor model and ensure it stands up to regulatory scrutiny.

.jpg)

.jpg)

.jpg)